Understanding Amortization Schedules: Calculation, Formulas, and Examples

Introduction:

Amortization schedules play a crucial role in financial planning, particularly in the realm of loans and mortgages. This article will delve into what an amortization schedule is and how it can be calculated using specific formulas. With a focus on the USA geography, we’ll explore the concepts of average collection period, cash books, cost of debt and equity, cost-volume-profit analysis, current account, days payable outstanding, depreciation, EBITDA, economic order quantity, factors of production, fiscal year, general ledger, just-in-time inventory management, net operating loss, net realizable value, and more.

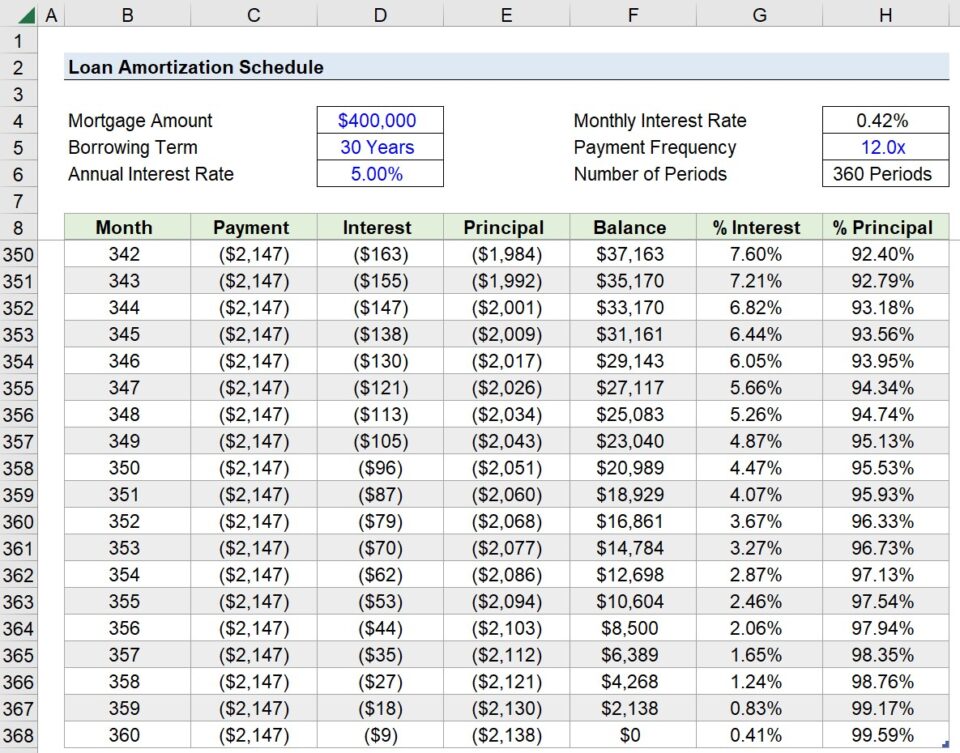

1. Amortization Schedule: Definition and Calculation

An amortization schedule is a table that illustrates the repayment of a loan over a specific period. It breaks down the monthly payment into principal and interest components. To calculate an amortization schedule, you can use the following formula:

Amortization Payment = Principal Amount [r(1+r)^n]/[(1+r)^n-1]

Where:

- Principal Amount is the initial loan amount

- r is the monthly interest rate

- n is the number of payments

2. Understanding Average Collection Period and its Formula

The average collection period is a key metric for a business, indicating the average number of days it takes to collect payments from customers. This measurement reflects the effectiveness of the company’s credit and collection policies. The formula for average collection period is:

Average Collection Period = (Accounts Receivable / Total Credit Sales) * Number of Days

Example: Let’s say a company has accounts receivable of $50,000 and total credit sales of $200,000 over a year. It has 365 days in the year. Calculating the average collection period:

Average Collection Period = ($50,000 / $200,000) * 365 = 91.25 days

3. Understanding the Importance of a Bill of Lading

A bill of lading is a legal document issued by a carrier that details the shipment of goods from the point of origin to the destination. It serves as a receipt, a contract, and a title document for the goods being transported. There are various types of bill of lading, including straight bill of lading, order bill of lading, and negotiable bill of lading. Let’s consider an example to better understand its purpose:

Example: A shipment of goods is transported from New York to Los Angeles. The bill of lading outlines the specifics of the cargo, such as quantity, weight, and packaging. It ensures that both the shipper and the carrier are aware of their responsibilities and liabilities during transit.

4. The Significance of Cash Books and How They Work

Cash books serve as a record of a company’s cash transactions, enabling accurate management of funds. They typically include columns for receipts, payments, and a running balance. Cash books provide a clear overview of cash inflows and outflows, making it easier to monitor cash flow. Let’s examine an example:

Example: XYZ Company maintains a cash book to record its daily cash transactions. It records cash inflows from customer payments and cash outflows for expenses like rent, utilities, and salaries. At the end of each day, the cash book’s running balance is updated, ensuring accurate financial management.

5. Understanding the Cost of Debt and How to Calculate It

The cost of debt is the cost a company incurs by borrowing funds through loans, bonds, or other debt instruments. It is the interest expense paid by the company on its outstanding debt. To calculate the cost of debt, you can use the formula:

Cost of Debt = (Interest Expense / Total Debt) * 100

Example: Suppose ABC Corporation has an interest expense of $500,000 and total debt of $10 million. Calculating the cost of debt:

Cost of Debt = ($500,000 / $10,000,000) * 100 = 5%

Other references:

- Investopedia – Amortization

- Calculator.net – Amortization Calculator

- Educba – Amortization Formula

- LeaseQuery – Lease Liability Amortization Schedule in Excel

- Rocket Mortgage – Mortgage Amortization

- Indeed – How to Calculate Amortization

- Wall Street Prep – Loan Amortization Schedule

- Ablebits – Create a Loan Amortization Schedule in Excel

- Deskera Blog – Amortization

- Bankrate – Amortization Calculator

Leave a Reply